WHY COGNIZANT WAS AT RISK OF LOSING TRACTION

Milestones

- 1994: Dun & Bradstreet turned its IT team into an offshore joint venture called Dun & Bradstreet Satyam Software, with Srini Raju as CEO

- 1996: Turned the JV into an independent company called Cognizant Technology Solutions, with Kumar Mahadeva as CEO

- 1998: Venture went public

- 2000: Good traction

- 2003: Stormed into Fortune 100 Fastest-Growing Companies

What the Venture Had Going For It

- Kumar Mahadeva: Visionary founder with restructuring and capital markets capability

- Strong founding logic: US parent + India execution, Capitalized parent company’s customers, Capitalized low-risk, high-volume demand for maintenance work, Capitalized tech IPO craze

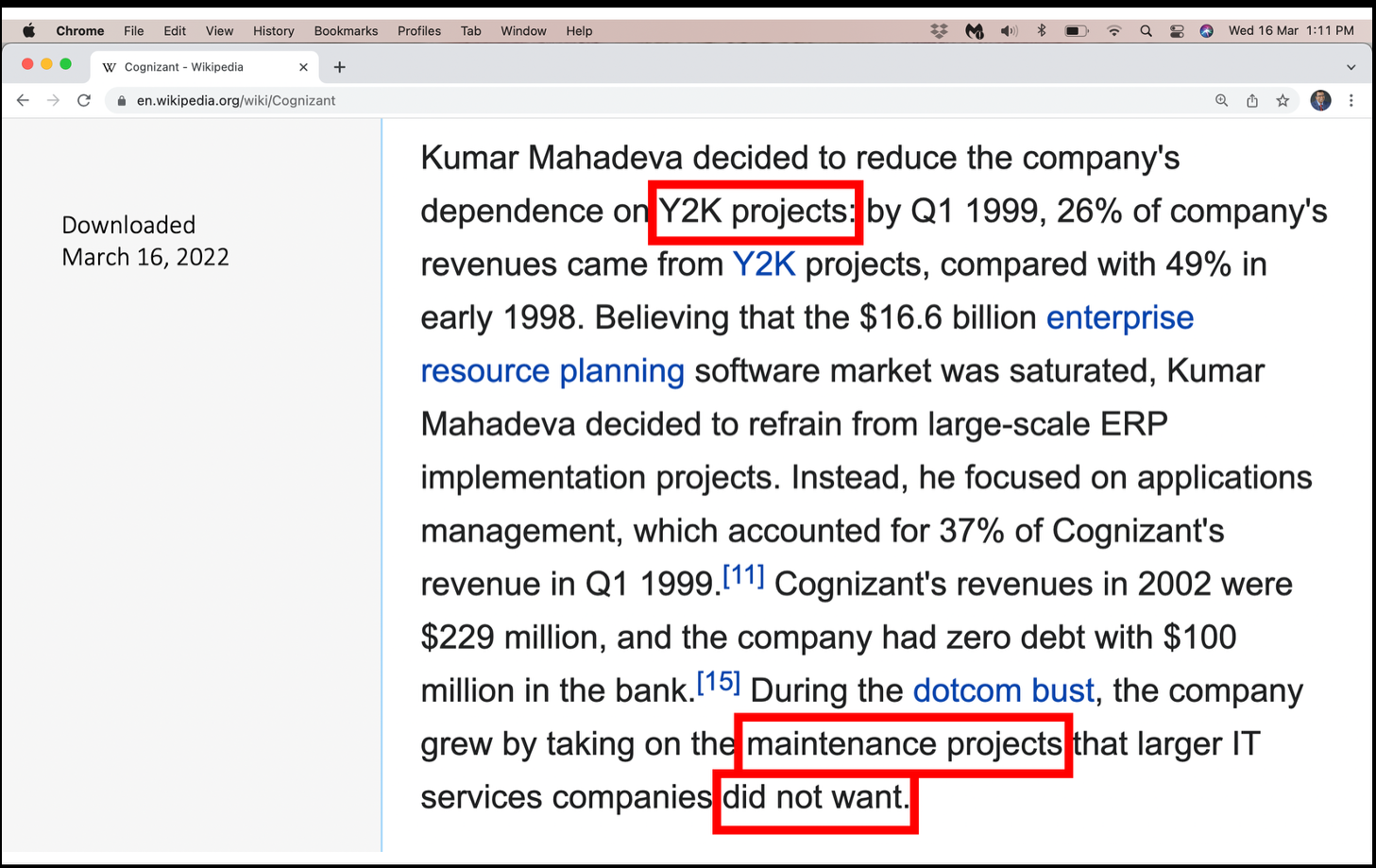

- Early good financial performance: Revenue doubled from $24.7M to $58.6M (1997-1998) and net income increased sixfold from $1M to $6M

- Demonstrated excellent technical and project management capabilities

- Clearly a promising venture as my offer letter said

What the Status Quo Model Actually Was

- Legacy maintenance / y2k expertise would exclude the venture from emerging-tech deals with Western enterprises and make it difficult to attract and retain high-end talent

- No user-centric design capability in India: user interfaces were pure mayhem — like the streets in India; no technical writing capability to soften the blow.

- Backlash on India's offshoring model — backlash targeted India’s lack of user-centric design capability. Read Offshore Usability

- Revenue concentrated in parent-venture relationship

- The venture operated during the tech bubble, which inflates valuations and creates unsustainable market expectations

- Corporate image: offshore labor-arbitrage

Questions

- Will Western enterprises trust such a venture with emerging-tech (web) projects?

- Will a “low-cost, body-billing” image work for a US venture – like it did for Indian companies such as TCS?

The Counterfactual: What If They Simply Tried to Scale That Model?

- Add more legacy maintenance contracts

- Expand body-billing capacity

- Compete on cost

- What happens when Y2K fades and web/digital rises?

Demand Shift Mismatch

Enterprise demand is moving toward: Web-based systems, Customer-facing applications, Integrated business solutions, and High-quality user experiences. A narrow engineering-only shop, focused on maintenance and backend work, operates in a commoditized segment and is structurally misaligned with where value is growing. Result: Limits the ability to capture high-value opportunities, slows growth, and constrains margins due to pressure from current and new low-cost competitors.

Client Portfolio Constraint

Heavy reliance on inherited customers and low-visibility projects limits the firm to transactional projects with no access to innovation budgets. Result: Plateauing of customer acquisition and growth-critical revenue.

Offshoring Backlash Amplified

With rising skepticism toward offshore labor, a “low-cost offshore coding shop” image limits access to high-value projects and strategic customer relationships. Lack of user-centric design and business-savvy amplifies the negative impact on customer acquisition and revenue growth, creating a structural ceiling on addressable market and ability to scale profitably.

So What Was the Real Risk?

Without structural change, the venture was at risk of being confined to low-value commoditized offshore execution, with constrained margin, reduced relevance, and an elevated probability of short-term plateauing and medium-term stagnation

You know the stakes. You therefore applaud the success more loudly. More importantly, you learn rare business lessons that you can actually use! You now crave to know whether structural change was done.

My Contribution to Cognizant's SuccessPHenry08@gsb.columbia.edu

© Pradeep Henry 2026